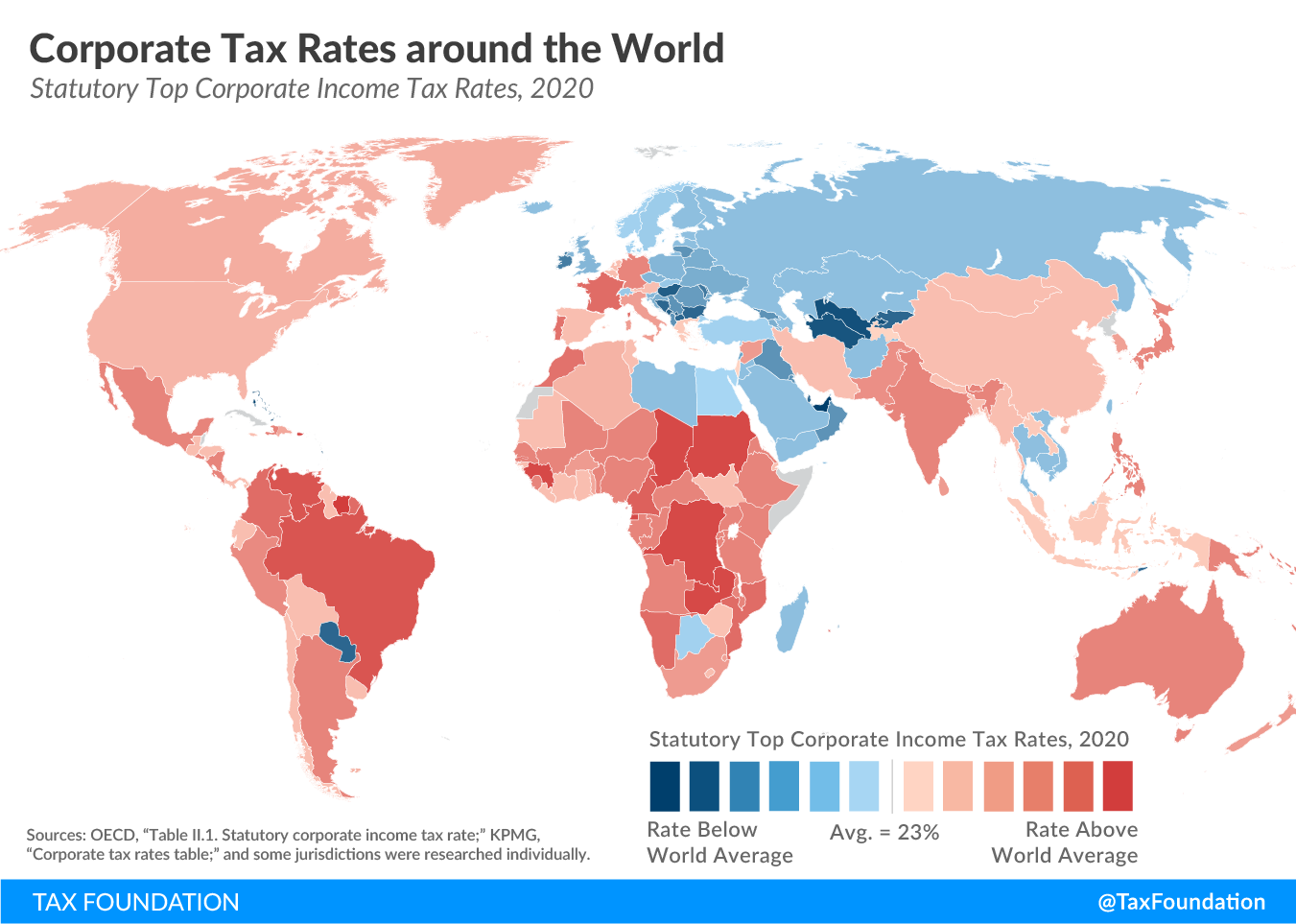

Corporate tax rates play a crucial role in shaping the economic landscape, influencing both revenue generation and business behavior. With the expiration of significant provisions from the 2017 Tax Cuts and Jobs Act looming in 2025, the debate surrounding these rates has intensified. In a recent analysis, renowned economist Gabriel Chodorow-Reich examined the impact of these tax cuts, revealing how they contributed to modest wage increases and business investments but ultimately led to a substantial decline in corporate tax revenue. As Congress stands divided on the issue, the implications of altering corporate tax rates could significantly influence the future of public funding and economic growth. Understanding these dynamics is essential for voters and policymakers navigating the complexities of fiscal policy in the upcoming election year.

The discussion around corporate tax rates is not only about numbers; it encapsulates broader economic principles that affect businesses and workers alike. Phrases like business taxation and fiscal revenue strategies are central to understanding the intricacies of how corporate decisions can drive their investments and, consequently, wage trends in the workforce. The Tax Cuts and Jobs Act, which renegotiated tax obligations for corporations, has been a focal point in evaluating economic health and corporate behavior. As we assess the fallout of such tax reforms, the insights provided by economists like Gabriel Chodorow-Reich become invaluable in shaping future policies. Crafting effective corporate taxation strategies will remain a pivotal theme as various stakeholders advocate for different approaches to foster economic growth and stability.

Overview of Corporate Tax Rates and Economic Impact

The discourse surrounding corporate tax rates has intensified as we approach the expiration of significant provisions stemming from the 2017 Tax Cuts and Jobs Act (TCJA). This legislation, hailed as a major overhaul of the U.S. tax system, reduced the corporate tax rate from 35% to 21%, which was a pivotal decision aimed at invigorating the economy. According to studies by economists, including Gabriel Chodorow-Reich, while the intent was to stimulate business investments and increase wages, the outcomes have been mixed, with corporate tax revenues suffering considerable declines in the immediate aftermath of the reforms.

As we analyze the impacts of these corporate tax revisions, it becomes evident that the landscape of wage increases and business investments doesn’t paint a broadly beneficial picture. Chodorow-Reich’s findings suggest that although corporate investments did rise by around 11% under the TCJA, the corresponding wage growth was significantly lower than anticipated. While proponents of the tax cuts often argue that such measures pay for themselves through increased investments, the initial steep decline in corporate tax revenue raises critical questions about long-term fiscal sustainability.

The Debate on Corporate Tax Increases

As election debates heat up, the conversation around potential corporate tax increases emerges as a contentious issue. With key provisions of the TCJA set to expire, lawmakers are revisiting whether raising corporate tax rates could be a viable solution to counteract the shortfall in tax revenues. Many Democrats, including Vice President Kamala Harris, advocate for higher corporate tax rates as a means to fund social initiatives, yet Republican leaders argue that lowering taxes further may catalyze growth and bolster business sentiments.

Amid this political tussle, Gabriel Chodorow-Reich emphasizes the necessity of reevaluating not only the statutory rate but also the broader implications of tax policy on business behaviors. His research reveals that while traditional statutory rate cuts have a certain universal appeal, targeted provisions such as immediate expensing of fixed investments yield more pronounced effects in stimulating economic activity. Therefore, any discussions around corporate tax increases must take into account the nuanced responses from businesses, and how different tax structures can shape overall economic health.

Corporate Tax Revenue Trends Post-TCJA

Following the implementation of the TCJA, corporate tax revenues initially plummeted, with a dramatic 40% reduction noted. Nonetheless, the subsequent years have shown a perplexing resurgence in corporate tax revenue, which began to outpace initial expectations by 2020 due to unforeseen spikes in corporate profits. Factors such as shifts in global supply chains and the evolving landscape of multinational corporations playing to lower tax rates significantly contribute to these trends.

One of the intriguing aspects highlighted by Chodorow-Reich’s analysis is the role of the pandemic in altering corporate financial dynamics. The surge in corporate profits amidst the TCJA’s implementation suggests that revisionist explanations around tax cuts stimulating immediate growth may not entirely account for nuanced economic behaviors during times of crisis. As lawmakers grapple with future policies aimed at corporate taxation, a keen understanding of these evolving patterns will be crucial for developing strategies that effectively balance tax revenue needs with incentives for growth.

Impact of the Tax Cuts and Jobs Act on Wage Growth

Proponents of the TCJA often promised substantial wage increases as a direct result of corporate tax reductions, forecasting annual boosts ranging from $4,000 to $9,000 per employee. However, contrary to these expectations, research by Gabriel Chodorow-Reich indicates that the actual wage increases have been more modest, estimated at around $750 annually. This divergence between predicted and actual wage growth underscores the complexities of corporate tax policies and their real-world effects on workers.

Such discrepancies highlight the critical role of understanding economic signals. If higher corporate taxes are viewed as a disincentive for investment, calls for reform must incorporate strategies to bridge the gap between corporate gains and worker benefits. The experience with TCJA suggests policymakers need to think critically about how tax policies are constructed to not only enhance corporate profitability but also ensure that these gains translate into meaningful wage increases for employees.

The Influence of Corporate Tax Policy on Business Investments

Business investments have been a focal point of discussions surrounding corporate taxation and economic stimulation. Gabriel Chodorow-Reich’s research emphasizes that the provisions allowing companies to immediately deduct the full costs of new capital investments led to a substantive 11% increase in business investments. Such targeted incentives demonstrate that corporate tax policy can play a critical role in shaping business decisions, guiding them toward immediate capital expenditures rather than relying solely on rate cuts.

Nonetheless, this relationship between tax policy and investments is not straightforward. While investment saw a favorable uptick, the fleeting nature of certain tax benefits raises questions about sustainable business growth. Therefore, as we consider future tax legislation, it’s essential to craft policies that not only incentivize short-term investment increases but also lay the groundwork for enduring economic expansion.

Revisiting the Effectiveness of Corporate Tax Cuts

The debate surrounding the effectiveness of corporate tax cuts as a driver of fiscal health and economic growth demands critical examination. While proponents argue that lower corporate tax rates encourage companies to reinvest in their operations, findings from Chodorow-Reich and colleagues present a more nuanced picture. Despite initial gains in investment, the corresponding decline in corporate tax revenues challenges the assertion that tax cuts will inevitably finance themselves through higher economic output.

In revisiting the TCJA and its implications, stakeholders must consider long-term strategies that prioritize not just corporate profitability, but also the broader economic ecosystem, including wage growth and public revenue. This perspective highlights the importance of a balanced approach, where businesses are incentivized to thrive while ensuring adequate funding for vital public services.

Partisan Perspectives on Corporate Tax Reforms

As corporate tax reforms become increasingly politicized, the divide between Republican and Democratic perspectives has grown more pronounced. While Republicans often champion tax cuts as a means to enhance economic freedom and stimulate growth, Democrats prioritize restoring higher tax rates to support social spending initiatives. The upcoming tax legislation debates signal a pivotal moment where contrasting ideologies will shape the trajectory of fiscal policy, particularly with the expiration of significant TCJA provisions in sight.

Gabriel Chodorow-Reich’s findings serve as a critical reminder of the need for evidence-based dialogue in these partisan discussions. Understanding not just the numbers but the underlying economic principles will be essential in crafting tax policies that fulfill both revenue goals and investment incentives. Such a balanced approach would ideally mitigate partisan extremes, allowing for a comprehensive reevaluation of corporate tax rates.

Future Considerations for Corporate Tax Legislation

Looking ahead, the paradigm of corporate tax legislation faces considerable challenges and opportunities. With key provisions from the TCJA approaching expiration and lawmakers contemplating future adjustments, discussions must reflect a synthesis of research findings and real-world economic dynamics. Exploring mechanisms that both enhance corporate responsibility and generate necessary revenue will be paramount in crafting effective tax policies.

Additionally, understanding the relationship between corporate taxation and wider economic trends will require input from a diverse array of stakeholders—including economists, businesses, and the public at large. As Gabriel Chodorow-Reich highlights in his work, the impact of tax policies extends beyond mere financial calculations, influencing everything from wage patterns to general economic growth, making informed dialogues on corporate taxation crucial for sustainable planning.

Evaluating Tax Provisions and Their Longevity

The trajectory of specific tax provisions under the TCJA, particularly those that allow immediate expensing, raises key questions about the longevity and effectiveness of such measures. As various elements face sunset clauses, evaluating which provisions truly drive economic growth versus those that merely offer temporary relief will be essential for future policy-making.

Chodorow-Reich’s analyses suggest that some tax benefits may yield better returns on investment than others. Such insights might encourage lawmakers to consider a tax framework that adapts more fluidly to evolving economic conditions, favoring provisions that sustainably stimulate investment over lowering statutory rates indiscriminately. This strategic approach could pave the way for a more resilient fiscal environment.

Frequently Asked Questions

What impact did the Tax Cuts and Jobs Act have on corporate tax rates?

The Tax Cuts and Jobs Act of 2017 significantly reduced the corporate tax rate from 35% to 21%. This major change aimed to stimulate business investments and economic growth, although it led to a notable decline in federal corporate tax revenue, estimated to be a loss of $100 billion to $150 billion annually over the next decade.

How did corporate tax rates affect corporate tax revenue after the TCJA?

After the implementation of the TCJA, corporate tax revenue initially plummeted by 40%. However, starting in 2020, there was a notable recovery in corporate tax revenue as business profits surged, exceeding initial forecasts.

Did the reduction in corporate tax rates under the TCJA lead to higher wages?

The reduction of corporate tax rates under the TCJA was expected to lead to significant wage increases. However, empirical studies, including those by Gabriel Chodorow-Reich, suggested a much smaller wage increase, estimating around $750 per year, contrary to prior forecasts of $4,000 to $9,000.

What lessons were learned from the corporate tax cuts under the 2017 Tax Cuts and Jobs Act?

One key takeaway from the TCJA is that while corporate tax policy does influence business behavior, the expected returns in terms of revenue and wage growth may be overstated. For instance, while capital investments did increase by about 11%, the significant drop in corporate tax revenue raised questions about the efficacy of such cuts.

How does the debate over corporate tax rates reflect on business investments?

The debate surrounding corporate tax rates often centers on their influence on business investments. Research has indicated that specific provisions allowing full expensing of capital investments were more effective in driving business investments than broad rate cuts, suggesting that targeted tax incentives could yield better economic outcomes.

What future actions are being discussed regarding corporate tax rates?

As the expiration of key provisions of the TCJA approaches in 2025, discussions are ongoing about potentially raising corporate tax rates while reinstating beneficial expensing provisions. This trade-off could create a new path for generating corporate tax revenue and incentivizing business growth.

Why is understanding corporate tax rates important for economic policy?

Understanding corporate tax rates is crucial for economic policy as they directly affect government revenue, corporate behavior, and, ultimately, wage levels for employees. Policymakers rely on data and research, such as those from Gabriel Chodorow-Reich, to inform decisions that balance the needs of businesses with revenue requirements for public spending.

| Key Point | Details |

|---|---|

| Corporate Tax Rate Changes | The TCJA reduced the corporate tax rate from 35% to 21%. |

| Impacts on Revenue | Federal corporate tax revenue was projected to decline by $100-$150 billion annually. |

| Wage Changes | Wage increases were modest, with estimates ranging from $750 to $9,000 per employee. |

| Investment Response | Investment increased by about 11%, primarily due to expensing provisions. |

| Political Debates | Republicans advocate for further tax cuts, while Democrats call for increases. |

| Future Tax Policies | Potential for changing corporate tax rates while restoring investment incentives. |

Summary

Corporate tax rates are currently under intense scrutiny as Congress approaches potential reforms in 2025. The Tax Cuts and Jobs Act (TCJA) in 2017 significantly lowered corporate tax rates, leading to both increased business investments and a notable drop in federal tax revenue. The debate continues as evidence suggests modest benefits to wage growth and varying impacts on overall economic health. As lawmakers gear up for discussions, the future landscape of corporate tax rates remains crucial for shaping fiscal policy and public sentiment.